How to file an insurance claim for car body repairs

How toInsurance claim filing processFile an Insurance Claim for Car Body Repairs: A Step-by-Step Guide

That sinking feeling of seeing a fresh dent or scrape on your car is stressful enough. Figuring out the insurance maze shouldn't be. Whether you found a mystery scrape at the grocery store or were involved in a collision, knowing the right steps can save you thousands in out-of-pocket costs.

At CrashFix, we help California drivers navigate the auto body claim process from start to finish. Here is exactly what you need to do to ensure your car is restored to factory standards.

Step 1: Document the Damage Immediately

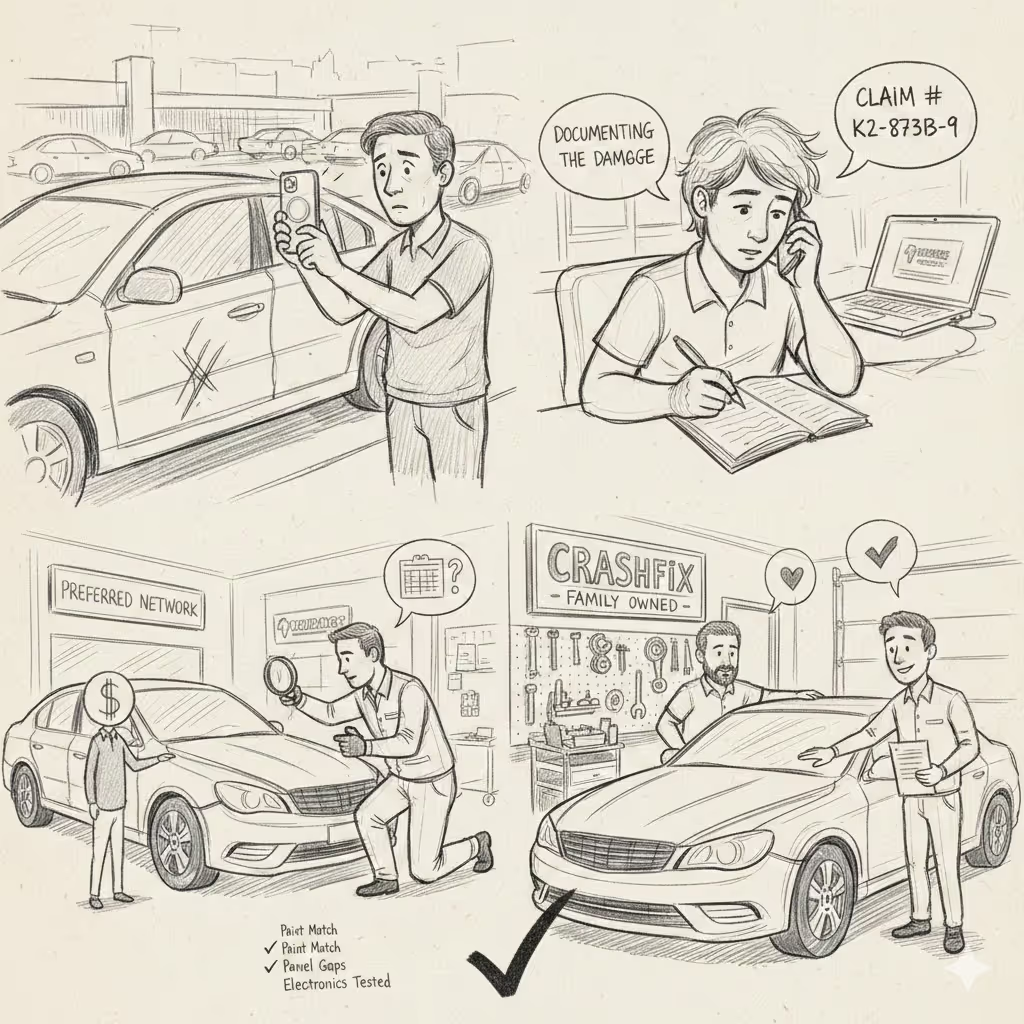

The most powerful tool for a smooth claim is in your pocket. Before moving the car or leaving the scene, create a digital record:

- Wide Shots: Capture the entire vehicle and its surroundings to provide context.

- Close-ups: Photograph the impact zone from multiple angles.

- Pro Tip: Capture the license plates of any other vehicles involved.

Step 2: Contact Your Insurer and Get a Claim Number

Call your insurance provider to report the incident. During this call, they will issue a Claim Number.

Important: This unique code is the "key" to your entire repair. It tracks everything from your initial estimate to the final payment.

Not sure if you should file? Contact CrashFix for a Claim Consultation first. We can help you determine if the repair cost exceeds your deductible before you notify your insurer.

What to Expect During the Insurance Adjuster Inspection

Once a claim is filed, an Insurance Adjuster is assigned to your case. Their goal is to document physical damage and estimate repair costs.

What they look for:

- Related Damage: They only inspect areas tied to the specific incident reported.

- Fresh vs. Pre-existing: Adjusters are trained to distinguish a new dent from an old rust spot or windshield chip.

- The Initial Estimate: They will provide a line-by-line report. Note: This is a "starting point." Adjusters rarely see hidden damage (like broken sensors or bent frames) until a body shop begins disassembly.

Can I Choose My Own Auto Body Shop? (Your Rights in California)

Yes. In California, it is your legal right to choose any licensed auto body shop. Your insurer may suggest a "Preferred Shop" (Direct Repair Program), but you are not obligated to use them.

Choosing between a preferred and an independent shop often comes down to where the shop’s loyalties and benefits lie. A Preferred Shop (DRP) typically maintains its primary loyalty to the insurance company, offering the convenience of streamlined billing and repairs that are usually backed by the insurer’s warranty. In contrast, an Independent Shop (like CrashFix) places its primary loyalty with you, the client. This independence allows them to provide comprehensive advocacy for high-quality parts and the peace of mind that comes with a lifetime warranty provided directly by the shop itself.

Since you have the right to choose your own repair facility, it’s important to have an advocate on your side before the first wrench turns. Book an appointment with CrashFix today for a Claim Consultation. We’ll help you understand your shop options, review your insurance estimate, and ensure your vehicle is restored with the quality and care you deserve—not just what the insurance company wants to pay for.

Understanding "The Supplement": What if the Estimate is Too Low?

It is very common for the initial insurance check to be lower than the shop’s quote. This happens because modern cars have complex sensors and brackets hidden behind plastic panels.

The Solution: When we disassemble your car and find more damage, we file a Supplement. This is an official request for additional funds. You do not need to manage this—CrashFix handles all negotiations with your insurer for you.

OEM vs. Aftermarket Parts: What’s Going on Your Car?

The parts used in your repair significantly affect your car’s resale value and safety.

- OEM (Original Equipment Manufacturer): Parts made by your car’s maker (e.g., Toyota, BMW).

- Aftermarket: "Generic" parts made by third parties.

- LKQ (Like Kind and Quality): Used, salvaged OEM parts.

Check your policy: Some insurance policies only cover OEM parts for new vehicles. If your policy specifies aftermarket parts, you can often pay the "price difference" out-of-pocket to upgrade to OEM. Ask your adjuster: "What type of replacement parts does my policy cover?"

Final Step: Paying Your Deductible and Inspection

When the work is done, you will pay your deductible directly to the auto body shop. Before driving away, perform this Quality Control Checklist:

- Paint Match: Check the color in direct sunlight; it should be seamless.

- Panel Gaps: Ensure the spaces between doors and fenders are perfectly even.

- Electronics: Test your blinkers, parking sensors, and cameras.

- Cleanliness: Your car should be returned cleaner than you left it.

Take Control of Your Claim with CrashFix

Filing an insurance claim shouldn't feel like a second job. At CrashFix, we provide expert consultations to ensure your vehicle is repaired safely and your premiums are protected.

Don't guess—get the facts. Schedule Your Claim Consultation Today.